In Sub-Saharan Africa, adults may also need to show ID to receive government benefit payments or to register their children for school.

“Can you please show me your ID?”

This is a question that people around the world hear every day as they run errands, like buying a SIM card or opening a bank account. In Sub-Saharan Africa, adults may also need to show ID to receive government benefit payments or to register their children for school. Without an ID, people often find themselves shut out from basic services, like opening a bank account, getting a loan, or even buying a SIM card. Even for making payments, they might be stuck carrying cash—risking theft—or taking time off work just to transfer money in person. All of this adds up, lack of ID can make it harder to access essential services that enhance economic mobility and security in their daily lives. Legal identity has been prioritized as an SDG target and many governments are exploring the potential of national ID systems—including digital ID. Digital IDs are becoming increasingly prevalent as governments transition to online verification systems. This form of national identification can help overcome the barriers of cost and distance. With standards and regulations, digital IDs can also reduce the risk of cyber theft and provide a secure, convenient way to access online services and payments.

Uganda, for example, saved around $7 million in a single year by using a national identification database to verify the identities of its civil servants. Malawi saved $44 million by merging its voter registration and national ID systems.

Despite this potential for economic and efficiency gains, access to a government-issued ID continues to be uneven across the African continent – limiting access to government services and digital platforms, which are foundational enablers of financial inclusion.

This blog provides an overview of ID ownership in Sub-Saharan Africa, drawing on survey data from randomly selected adults in 36 countries. This research is a collaborative effort between the World Bank’s Global Findex and Identification for Development (ID4D) Initiatives which have collected two rounds of global data on access and barriers to ID ownership since 2017. The most recent data find that an estimated 850 million people around the world do not have official identification—primarily people in lower-income countries and marginalized and vulnerable groups, of which approximately 470 million are in Sub-Saharan Africa. Here we look at some of the key trends in the region.

ID access varies by country in Sub-Saharan Africa

In the 36 Sub-Saharan African economies surveyed in 2021 and 2022, an average of 78 percent of eligible individuals over the age of 15 own an ID (Figure 1). The Global Findex collects data on adults aged 15+ but, in some economies, individuals are not eligible to have an ID until they are older than 15. Adults below the age cutoff are excluded from ID ownership calculations.

There are significant differences by country. In 13 economies, less than 70 percent of adults have an ID. Access gaps based on gender, income, and rural residency are particularly pronounced in lower-access economies, further excluding these vulnerable groups from accessing basic services such as receiving financial support from the government, applying for a job, or using financial services.

Figure 1: Access to a Government-issued ID varies across Sub-Saharan Africa

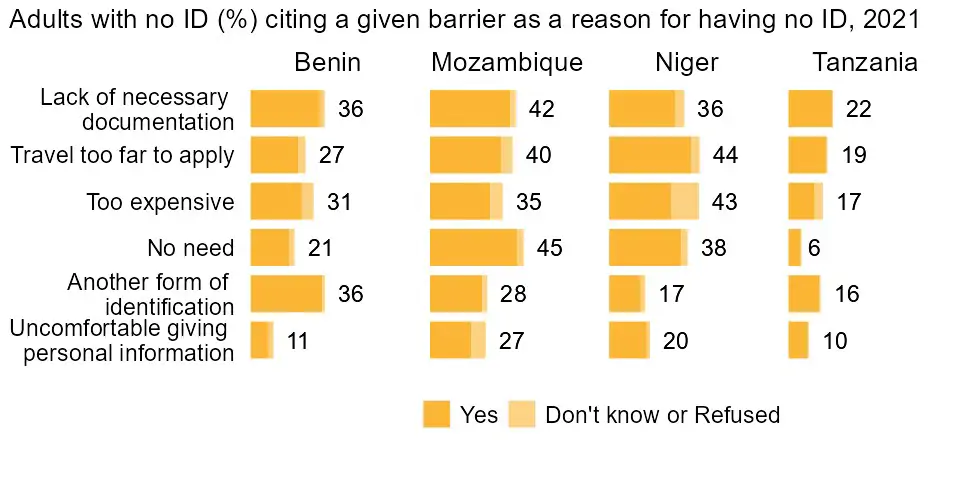

Distance and costs create barriers to ID access

When we asked adults without an ID why they don’t have one, the most common reason was that they lacked supporting documentation, like a birth certificate, needed to get one. They also mentioned that the distance they would have to travel to get one was too far. The expense of getting an ID is too high. Across the 13 countries with ID access lower than 70 percent, women are significantly more likely than men to report getting an ID as too expensive (see Figure 2), potentially due to higher cost and effort associated with obtaining supporting documentation and travel to register for or collect an ID. Data also show that 13 percent of adults without an ID in Niger don’t know or refuse to answer whether the services are expensive, implying that many might not even be aware of the costs associated with obtaining an ID.

Figure 2: Several barriers keep adults without an ID from getting one

ID access enables digital and financial inclusion—and lack of ID hinders it

The absence of an ID presents many challenges. For example, in 10 of the 13 economies with ID ownership below 70 percent, affected adults can’t buy a SIM card. This hinders digital connectivity, as a SIM card is essential for using a mobile phone. In Tanzania, 57 percent of adults with no ID (a quarter of all adults) experience this challenge. Without an ID, people found it difficult to vote, open a financial account, find a job, and receive medical care.

Over 30 percent of adults with no ID in Benin, Republic of Congo, The Gambia, Liberia, Mali, and Mozambique said it made them unable to access financial services. When unbanked adults in Sub-Saharan Africa were asked what keeps them from getting an account, 57 percent named insufficient documentation (including IDs), as a barrier. This latter point highlights the fact that ID is not the only documentation barrier unbanked people face (Figure 3). Financial providers often need additional documentation such as utility bills to fulfill customer due diligence) requirements. As a result, even people with a national ID may still be unable to open a financial account.

Figure 3: Many unbanked adults name lack of documentation (including ID) as a barrier to account ownership

Digital ID addresses some access barriers, but questions remain for Sub-Saharan Africa

Sub-Saharan African lags behind other regions in the adoption of advanced digital ID capabilities, as illustrated by recent data from the ID4D Global Dataset.

Furthermore, we don’t know whether adults in Sub-Saharan Africa will trust these digital systems once they are implemented. To address that knowledge gap, the Global Findex / ID4D collaboration is introducing new questions on digital ID ownership as part of the Global Findex 2024 survey. One goal is to collect gender-disaggregated data on identity theft and the unauthorized use of identity information for illicit activities.

These insights will lay the groundwork for more effective strategies to enhance ID access, digital connectivity, and financial inclusion, including gender-aware digital public infrastructure (DPI) initiatives.

To see our full policy note on this topic, Trends in Access to ID in Sub-Saharan Africa, visit the Global Findex Africa page. For global analysis of official government data on ID, see the ID4D Dataset.