The fintech industry is working to create a more equitable global financial system. Image: Unsplash/Edi Kurniawan

This article is part of:Centre for Financial and Monetary Systems

- Growth in the fintech sector is stabilizing and financial performance remains strong, according to a new World Economic Forum report.

- The survey of 240 fintech firms contains insights on this evolution and what it means for individuals and businesses.

- The report highlights fintech’s continued role in expanding financial access to traditionally underserved market segments including small businesses and low-income populations.

In recent years, fintechs have become integral to the financial system and today the industry is transitioning into a phase of sustainable growth, new data shows.

The second edition of the World Economic Forum’s The Future of Global Fintech: From Rapid Expansion to Sustainable Growth report, which was produced in collaboration with the Cambridge Centre for Alternative Finance, finds that after a surge during the pandemic, average fintech customer growth, driven by customer demand, is stabilizing at 37%. Financial performance remains strong, with revenue and profit growth at 40% and 39% respectively.

The report examines this landscape and the challenges and opportunities for fintechs as they continue to evolve, navigating macroeconomic instability, a regulatory landscape that is supportive but contains challenges and technological advances including artificial intelligence (AI).

Have you read?

- Why we must transform technical assistance to accelerate sustainable finance in emerging markets

- Why financial inclusion is the key to a thriving digital economy

Meanwhile, the data demonstrates the important role fintechs are playing in expanding financial access, with traditionally underserved groups including micro, small and medium enterprises (MSMEs) and low-income populations making up a large percentage of their customer base.

The report surveyed 240 fintech companies across the globe in six retail-facing sectors – digital lending, digital capital raising, digital payments, digital banking and savings, insurtech and wealthtech.

Here are some of the ways they are embedding accessibility and reach into their business models, helping to create a more equitable global financial system.

Targeting underserved customer groups

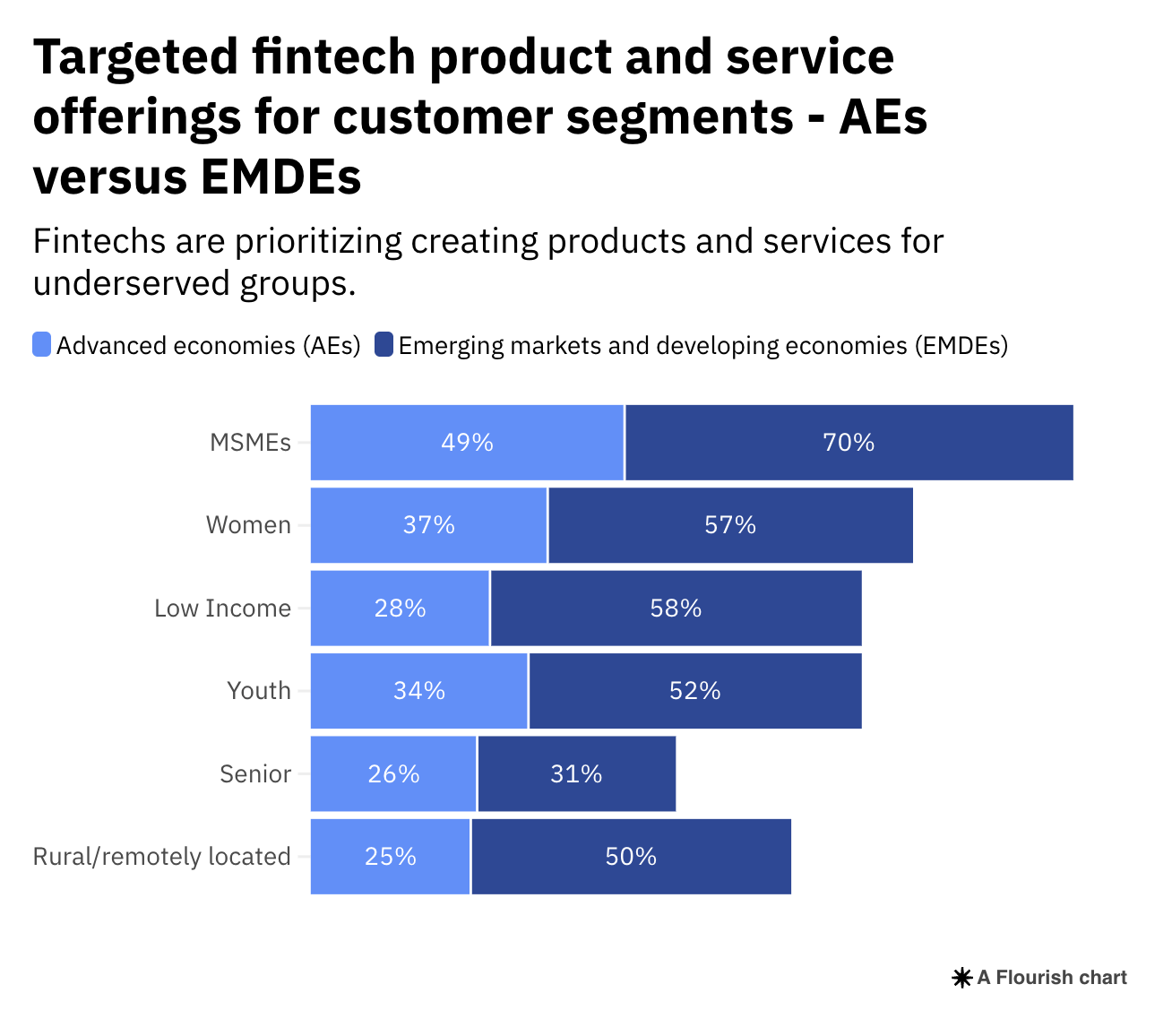

Worldwide, fintechs are continuing to prioritize underserved customer groups with targeted product and service offerings, especially for MSMEs, women, and low-income and youth customer segments.

Year-on-year, most underserved customer segments saw either steady or increased offerings – most notably MSMEs, with an increase from 48% in 2022 to 58% in 2023.

Emerging markets and developing economies (EMDEs) have a particular focus on MSMEs, with 70% of fintechs having offerings for this group. Overall, fintechs operating in EMDEs report having a larger percentage of products for underserved customers.

Strengthening digital focus

Globally, fintechs are increasing their digital focus as they expand their customer bases.

Most firms report relying on social media platforms, websites and referrals as primary customer acquisition channels, while traditional methods such as text messages and calls are declining.

Social media was a particularly prominent strategy in Latin America and the Caribbean (87%), Asia-Pacific (84%) and the Middle East and North Africa (83%). Across verticals, social media and referrals remained the most popular customer acquisition strategies.

The rise of open banking, open finance and digital public infrastructure, meanwhile, has been a “significant milestone” for the fintech sector, the report says. By allowing people to securely share their data with trusted third parties to access services that help them better manage their finances, these advances are creating new opportunities for innovation, market expansion and competition.

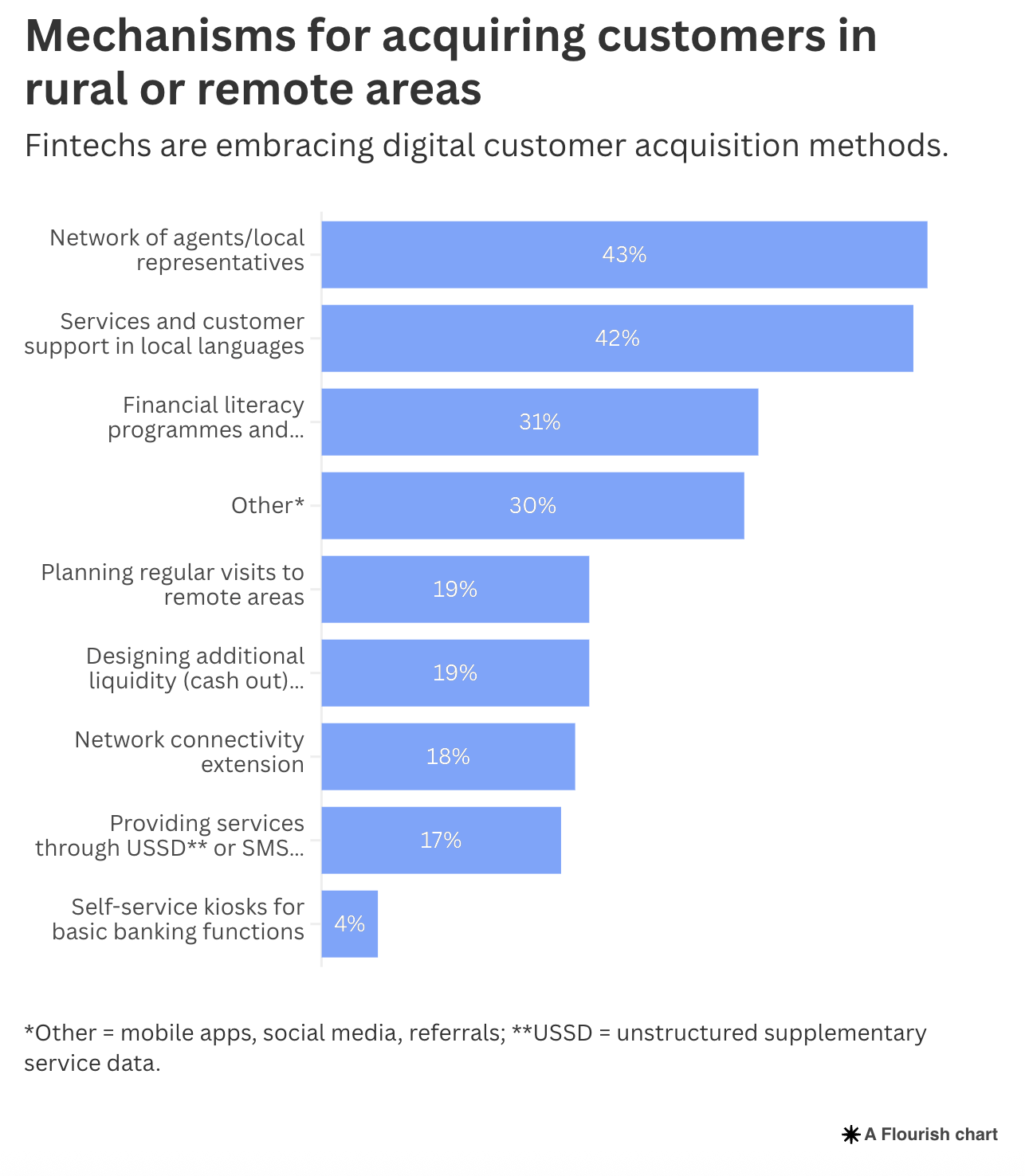

Using tailored approaches for customer acquisition

While digital is a growing focus for fintechs globally, in EMDEs digital methods can’t be the only approach – just 35% of people in developing countries have internet access.

As such, fintechs in these countries are employing multiple acquisition strategies, particularly for rural areas. These include individualized and tailored approaches including agent networks, multilingual services and financial literacy programmes.

Firms in Sub-Saharan Africa lead in outreach to rural customers, with a diverse range of strategies that includes the above approaches and providing services through channels such as SMS text messaging.

Adopting AI

Fintechs are actively investing in AI to enhance customer experience, improve operational efficiency and drive cost savings.

In total, 80% of the firms surveyed say they are implementing the technology across multiple business domains, led by customer service and process automation. Over a quarter were using AI in all five areas studied.

This widespread adoption is paying off, firms report, improving customer experience, reducing costs and boosting profitability.

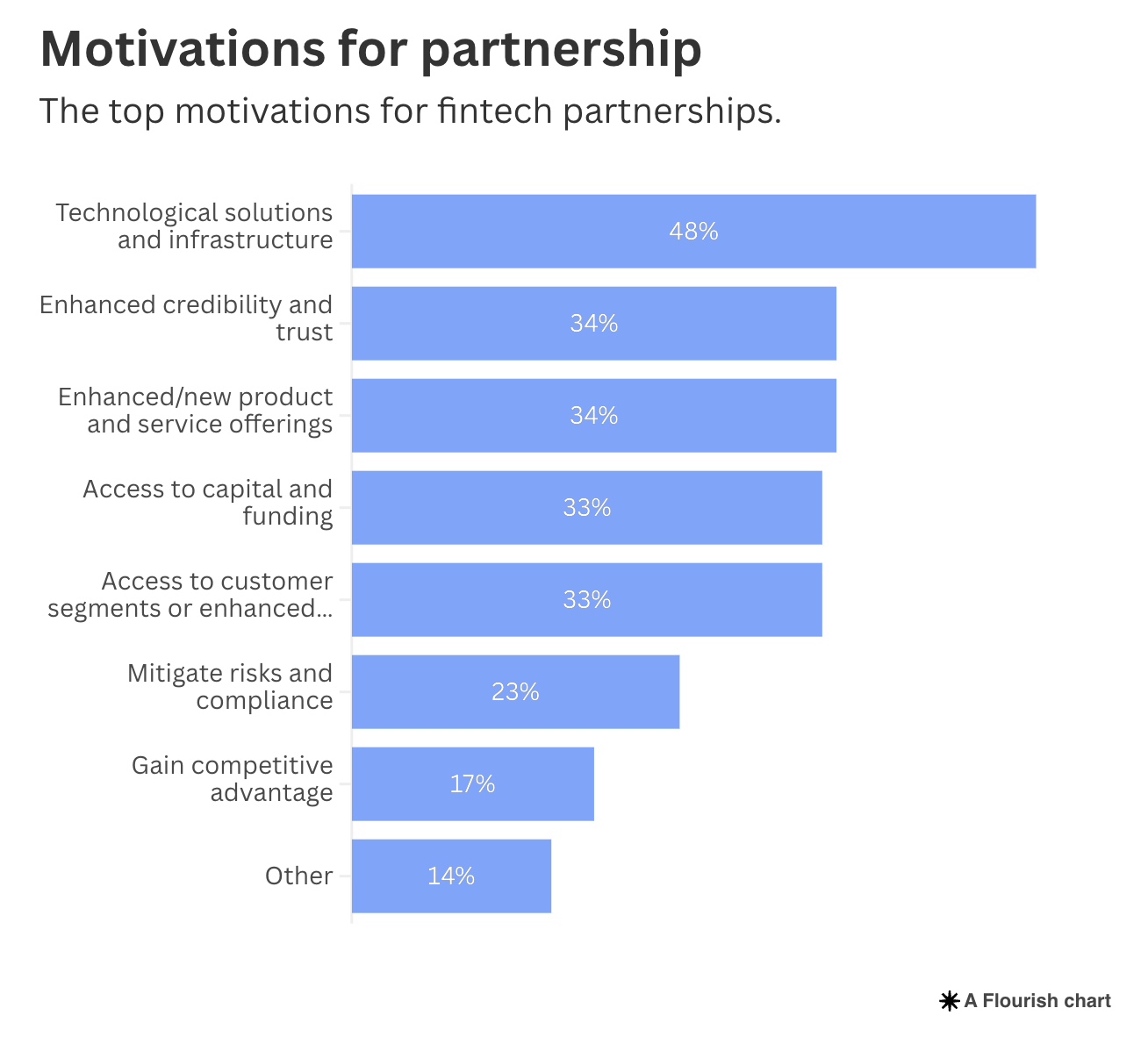

Embracing partnerships

Collaboration is playing a critical role in fintech strategies, with 84% of the firms surveyed partnering with incumbent financial institutions.

The primary motivations for these partnerships are technology solutions and infrastructure, enhanced credibility and trust, and product and service innovation.

The emphasis on trust and credibility is especially relevant in EMDEs, the report says, given that fintechs in those markets serve a higher proportion of underserved segments through targeted product offerings.

As the sector continues to evolve, insights such as those in the Forum report can support public and private sector leaders in their decision-making as greater public-private collaboration will be key to ensuring fintech reaches its full potential, ultimately helping develop an equitable, efficient and resilient financial system.

For more insights from the Forum's Centre for Financial and Monetary Systems, see here.

RELATED NEWS