New analysis of the Findex database reveals a striking generational and geographic divide in digital financial inclusion. | © Shutterstock.com

Picture two grandmothers, both in their late sixties, heading to their local market on a Monday morning. One in Ulaanbaatar, Mongolia, taps her phone to pay for vegetables, checks her government pension in an app, and heads home. The other, in Manila, counts out banknotes, as she has done her whole life. Her phone, if she has one, stays in her pocket.

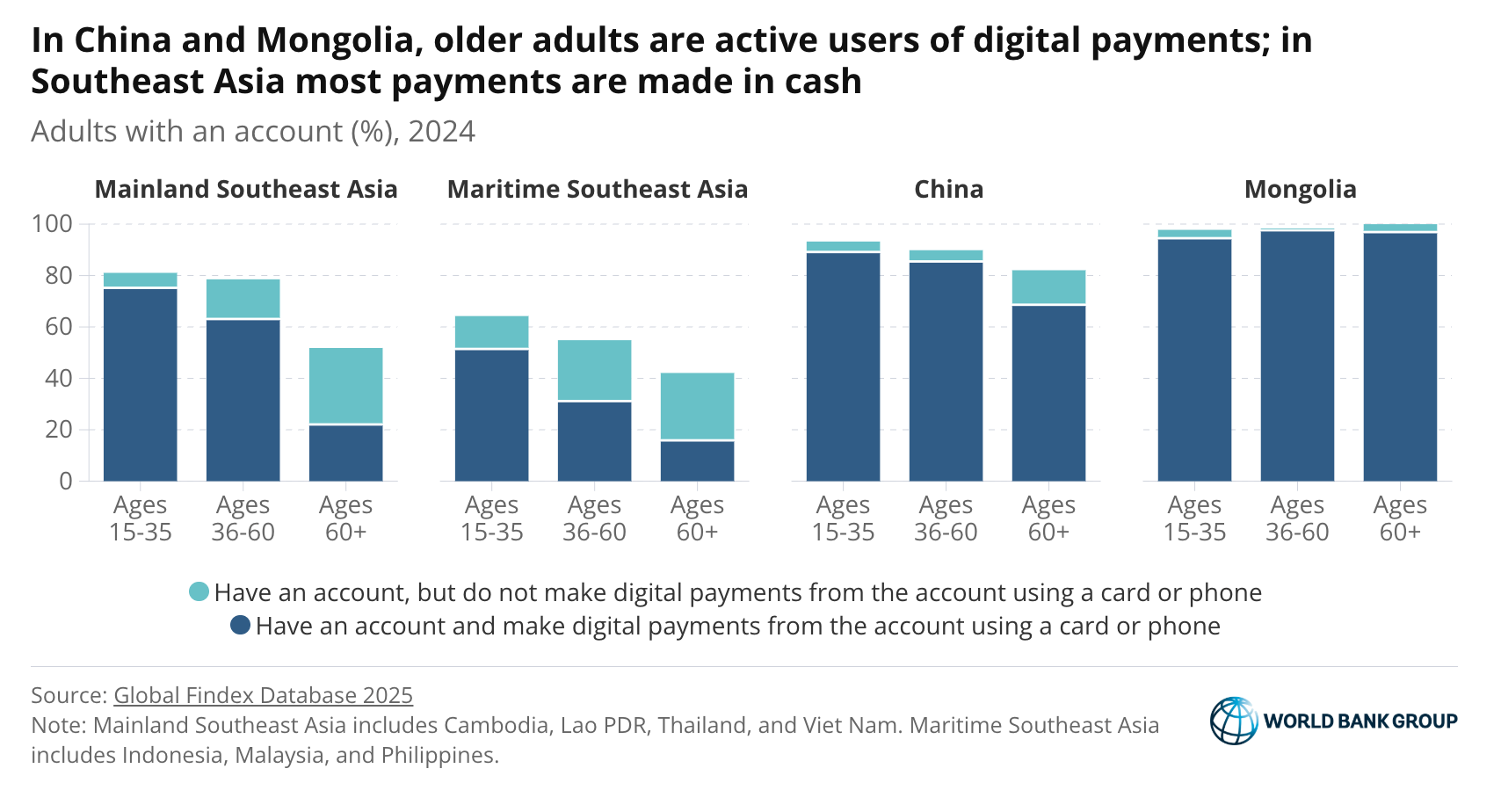

This contrast is not anecdotal. It reflects one of the most revealing patterns in the Global Findex 2025 database, based on nationally representative surveys across more than 140 countries. In Mongolia, about 90% of adults aged 60 and older make digital merchant payments. In the Philippines and Indonesia, that figure is close to zero.

New analysis of the Findex database reveals a striking generational and geographic divide in digital financial inclusion—and what it means for the world’s fastest-aging region.

A region getting older, fast

East Asia and the Pacific is aging faster than almost any other region in the world. By 2050, one in four people will be over 60. How this generation engages with digital financial services will shape individual well-being and broader economic resilience. Yet the Findex data makes clear that the region is not on a single trajectory.

High digital adoption in China and Mongolia

Older adults in China and Mongolia are among the most digitally included in the world, with account ownership among those over 60 rising sharply since 2014.

China’s story is well known. Platforms such as WeChat Pay and Alipay built payment ecosystems so ubiquitous that opting out became socially and practically difficult for any age group.

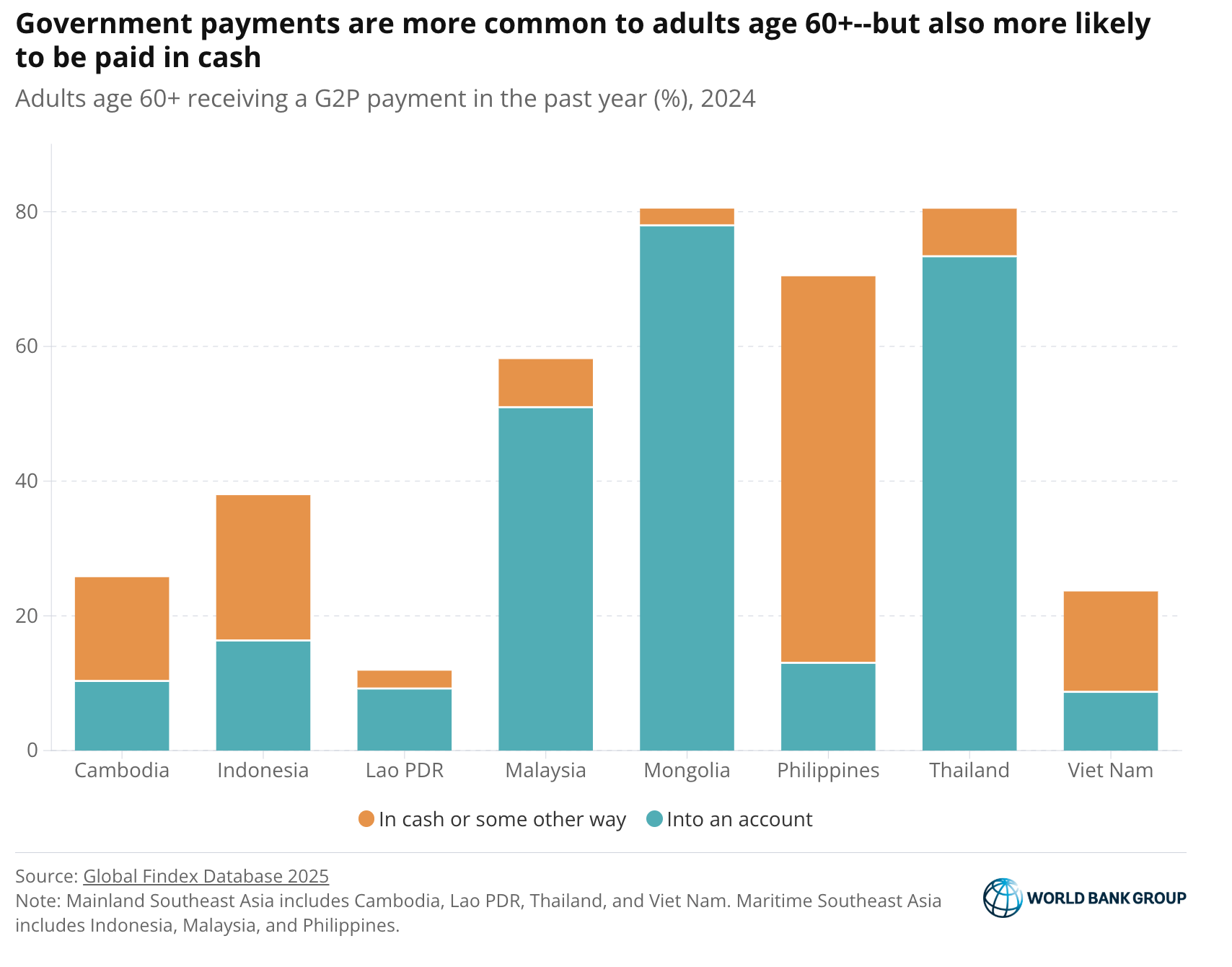

Less recognized is the role of government payments. In countries such as Malaysia, Mongolia, and Thailand, pensions and transfers are almost universally deposited directly into accounts. Rather than traveling to a branch or ATM to withdraw cash, many older adults use these funds directly to pay merchants for everyday purchases.

Yet in Indonesia, the Philippines, and Viet Nam, many older adults still receive transfers in cash—highlighting a missed opportunity to make government payments faster, more affordable, and better governed, and to use them as a bridge to digital financial inclusion. But even where accounts exist, usage does not automatically follow.

Lower digital adoption in Southeast Asia

This gap between access and usage is most visible in Maritime Southeast Asia. In Indonesia and the Philippines, mobile money, often linked to a bank account, is expanding financial access, but mainly for younger adults. For adults under 35, mobile wallets such as GCash in the Philippines or GoPay in Indonesia have enabled millions to open accounts and use digital payments. Among older adults, however, mobile wallet adoption remains small.

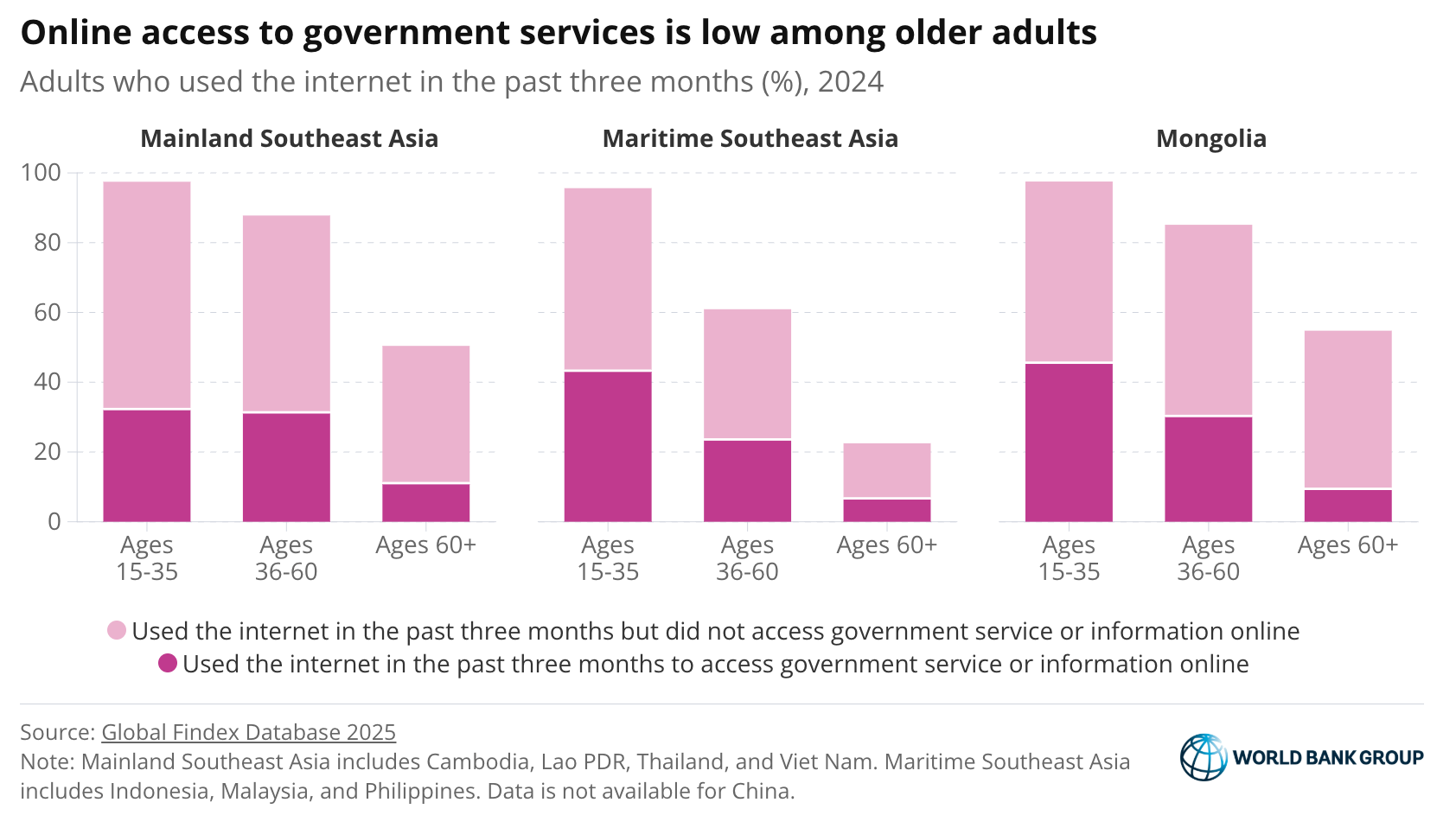

Limited digital access is a key barrier. In Indonesia and the Philippines, fewer than one in four adults over 60 use the internet, and across the region their usage rates are roughly half those of younger cohorts. Without reliable and affordable connectivity and basic digital skills, even well-designed digital payment systems remain out of reach.

This gap extends beyond payments. Older adults are also less likely to access government services online, despite often having greater need for healthcare and social protection.

Financial resilience is low among older adults

Even where older adults have accounts, financial resilience is limited. Across much of the region, most adults over 60 could cover no more than two months of expenses if they lost their income; in parts of Mainland Southeast Asia, many could not manage even two weeks. Informal safety nets - borrowing from family and friends or community-based savings groups - remain the primary fallback, especially for healthcare costs.

This underscores a broader point: financial inclusion does not automatically translate into greater financial health.

Supporting Aging Populations through Digital Financial Inclusion Policies: Lessons from the Republic of Korea

Younger generations already have higher levels of digital access and will carry these skills into older age. The more immediate challenge is ensuring that today’s older adults are not left behind in the transition to digital finance.

Consumer protection is critical. Older users of digital financial services, particularly pension recipient, must be able to transact safely and be protected from fraud, which has disproportionately affected older adults in countries such as Thailand. Equally important is design: user-friendly digital interfaces tailored to the needs and circumstances of older adults are essential for safe usage.

A new World Bank report, Supporting Aging Populations through Digital Financial Inclusion, shares policy lessons from the Republic of Korea to help address these challenges.

The goal is not simply to expand digital financial services, but to ensure they translate into greater financial security and resilience in older age.