Photo: Lakshmiprasad S from Getty Images

India’s digital payments journey has reshaped global imagination. At a moment when many countries still viewed fast payments as tools for high-value bank-to-bank settlement, India reimagined them as a universal service built for people and everyday life. That vision fundamentally reshaped understanding how payments could improve lives.

Earlier innovations had revealed the power of instant, everyday digital payments. Mobile money systems across emerging markets showed how simple, real-time, phone-based transactions could catalyze digital payment adoption for households and small businesses, particularly where banking access was limited. However, most mobile money models were provider-centric, and not interoperable. India’s contribution was to reframe instant payments as an open and interoperable infrastructure and make the system work better for people.

Today, more than one hundred jurisdictions operate fast payment systems, many drawing inspiration from India’s experience. In Latin America and the Caribbean, a new World Bank report analyzing data from eleven countries shows that fast payments are now driving the growth of digital payments in the region, accounting for forty-five percent of all digital payment volume in 2024, up from two percent in 2017.

Fast payments became universal

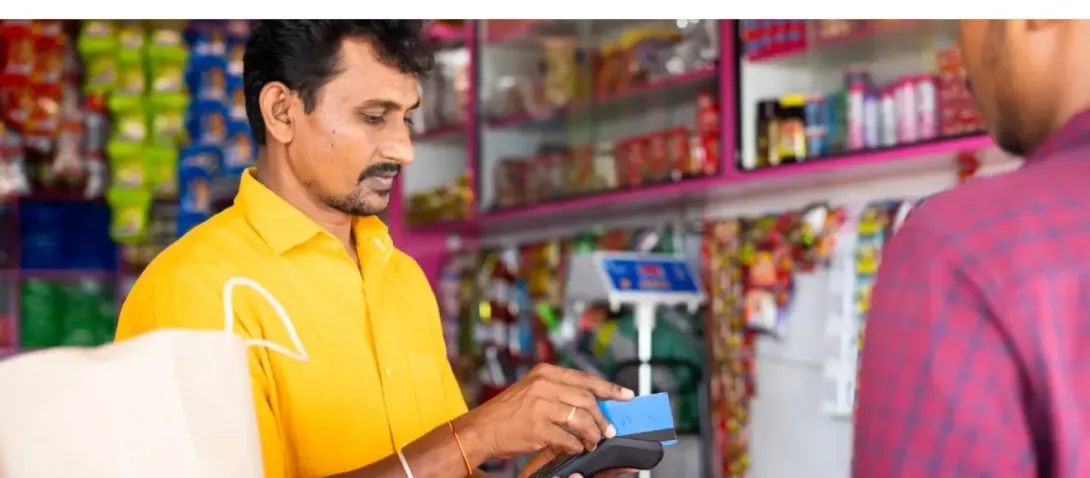

UPI (Unified Payments Interface) demonstrated that fast payments could be embedded into every kind of retail transaction. From paying a street vendor to settling online purchases to subscribing for initial public offerings of stocks, India demonstrated how fast payments could be a universal service accessible to everyone. It also proved that real-time payments can operate at population scale, serving every user and every use case.

UPI made digital payments feel like cash for the user: instant, universally accepted, and free at the point of use. But it removed cash’s constraints. People do not need to be in the same place. There is no shortage of change to complete a transaction, and the physical risk of money being lost, stolen, or destroyed disappears.

This expansion was made possible by designing UPI as an interoperable system that fully integrated both banks and non-banks, enabling third-party providers to innovate on top of common rails and dramatically accelerate adoption and merchant acceptance. By combining the trust and infrastructure of banks with the innovation speed of fintechs, UPI unlocked the scale and reach needed to transform retail payments nationwide.1

Across July to September 2025, UPI processed about fifty-nine billion transactions, more than Mastercard’s global total of roughly fifty-four billion and approaching Visa’s eighty-two billion worldwide. When compared to other fast payment rails, the scale of UPI is remarkable. In 2024, fast payment systems in the eleven LAC countries analyzed by the World Bank, including Brazil’s successful Pix, processed a combined total of 79.8 billion fast payment transactions, while UPI alone processed 172.2 billion transactions in the same year.

Today, more than eight out of ten digital payments in the country are initiated through this ecosystem, with over 504 million unique users, roughly half of India’s adult population, and more than 65 million merchants accepting UPI payments. The idea of real-time payments for all has now become a global reference point.

Innovation shaped around people, not technology

By opening space for nonbanks and enabling third-party application providers to compete on user experience and innovation, India broke historical patterns where only banks could shape the digital payments landscape. This decision encouraged creativity, attracted millions of new users, and proved that inclusion and innovation can reinforce each other.

India placed user experience and open participation at the center. UPI showed that the real revolution was not technology alone but how technology is felt by people. Simple account identifiers, intuitive interfaces, QR codes, and merchant acceptance initiatives transformed digital payments from a technical option into a cultural norm. Adoption emerged because the system solved real frictions in everyday life.

New use cases have fueled much of the recent growth. Person-to-Merchant (P2M) transactions now account for sixty-four percent of UPI volumes, driven by categories such as groceries, restaurants, fuel stations, debt collection, and digital services according to NCPI. This growth has been powered by constant innovation across the UPI value chain, expanding both what users can do and how they do it. UPI has evolved from simple account-to-account transfers into a comprehensive platform, with advances ranging from diverse onboarding mechanisms to new experience layers such as conversational payments and tap and pay.

The next chapter is underway

As transaction volumes scale and new digital financial services emerge, India has an opportunity to extend its leadership by ensuring the ecosystem remains open, resilient, and competitive. Strengthening operational resilience, managing concentration risk to ensure healthy competition, improving transparency for end-users and advancing open finance in a way that protects users and fosters innovation will sustain momentum. There is now an opportunity to integrate broader financial information for more inclusive credit, to support MSMEs through better consent mechanisms, and to expand value added services built on trusted data.

The world is watching the next phase. The foundations are strong. The impact is global. The story is still being written.

To learn more about India’s financial sector, click here.