Gender disparities: 57% of men had a phone, compared to 46% of women.

WBG

Mobile Phone Technology Could Expand Equitable Access to Financial Services in Ethiopia

Data from the Global Findex Database indicate that the percentage of adults with bank accounts in Ethiopia has more than doubled since 2014 to reach 46%. However, despite this growth, financial equity in the population has decreased. In particular, there are significant disparities in account ownership based on gender, income, and education. As of 2022, women are 16 percentage points less likely than men to have an account, while adults in the poorest 40% of households face a 20-percentage point income gap. Additionally, there is a substantial education gap of 41 percentage points among adults with a primary education or less.

There’s also evidence that digital payments can increase an entrepreneur’s profitability by making financial transactions with customers, suppliers, and the government more convenient, safer, and cheaper. Even informal micro, small, and medium enterprises (MSMEs) can build a sales and credit history to improve their access to credit. Yet in Ethiopia, 47% of self-employed adults have an account, as compared to 82% of wage workers (and 33% of adults who are out of the workforce).

Data show gaps in bank account ownership in Ethiopia

Source: Global Findex Database 2021

Ethiopia falls behind its neighboring countries and regional counterparts like Kenya, Uganda, and Tanzania in terms of account ownership and usage. Not only is account access lower in Ethiopia, but usage rates, especially for digital payments, are also significantly lower. Only 42% of account holders—20% of adults—used their accounts for digital payments in the year prior to the Global Findex survey, far lower than the average digital payment adoption rate of 57% observed across all developing economies. Lower, even, than regional peers like Tanzania, where 96% of account holders (50% of all adults) used digital payments.

Given the existing equity gaps, and how Ethiopia compares with regional counterparts like Kenya, Uganda, and Tanzania in terms of account ownership, what short-term opportunities exist to equitably increase account ownership and expand their use in the country? Our recommendations are to expand access to technology and increase the use of payment digitalization.

How technology access relates to account ownership

Account ownership in Ethiopia is predominantly tied to traditional financial institutions, such as banks, credit unions, and microfinance institutions, rather than mobile money accounts, which are more prevalent in countries like Kenya, Uganda, and Tanzania, and across Sub-Saharan Africa as a whole. In fact, only 5% of account owners have a mobile money account in Ethiopia, significantly lower than the Sub-Saharan Africa average of 33%. Those who do have a mobile money account also tend to hold accounts with financial institutions, suggesting that Ethiopia faces unique barriers to reaching the unbanked with mobile money, in addition to more general account ownership challenges.

46% of adults in Ethiopia have an account, more than double the 22% in 2014

Source: Global Findex Database 2021

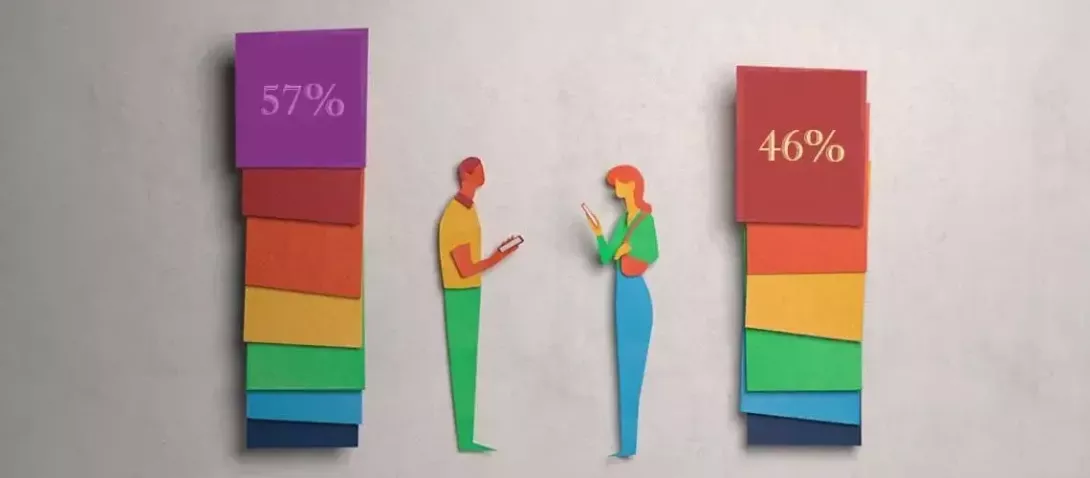

Data show that, when asked about the reasons for not having a mobile money account, 51% of unbanked respondents reported not owning a mobile phone. (This finding is supported by Gallup World Poll data which indicated that only half of Ethiopians had a mobile phone.) Again, gender disparities are evident; 46% of women had a phone, compared to 57% of men.

Not having a mobile phone is a common barrier to mobile money account ownership in Ethiopia

Other commonly reported barriers to mobile money account ownership include the lack of necessary documentation for account opening (such as an ID or address verification), distance to mobile money agents, and the perceived costliness of financial services. Similar obstacles are mentioned when respondents are asked about owning accounts at traditional financial institutions.

Source: Global Findex Database 2021 Note: Respondents could choose more than one reason.

How programs and policies that enable technology access and payment digitalization can drive account adoption and usage

Addressing technological and infrastructural barriers to financial inclusion presents a crucial opportunity. Implementing programs that improve technological access and promote mobile money agent networks as a viable alternative to brick-and-mortar financial institutions, as seen in neighboring economies, could effectively reduce the barriers of distance, cost, and technological access, thereby increasing mobile money account ownership rates in Ethiopia to levels comparable to its neighbors.

Furthermore, digitalizing payments has been associated with improved account access and use. In developing economies, over a third of adults (half of all account owners) opened their first account in order to be able to receive a government payment or wage. However, in Ethiopia, only 9% of adults (or one-fifth of account holders) did so, indicating low digital enablement by payers.

Nevertheless, there are indications that some payers are embracing the digitalization trend. In the year prior to the survey, one-third of adults receiving government payments did so digitally, surpassing the one-fifth share recorded in 2017.

Encouraging the adoption of digital payment methods can contribute to increased account ownership among unbanked adults. Similarly, there is potential for innovation in other payment types. Currently, only approximately 5% of adults who sell agricultural products receive their payments directly into an account—a rate that is unchanged since 2017. The remainder got paid in cash.

Embracing digitalization in a manner that allows payments to be sent directly to accounts, including to mobile money accounts, offers advantages for both payers and recipients. Governments and private sector payers have reported reduced costs, enhanced transparency, and fewer losses. Recipients, particularly the unbanked, benefit from a safer, more convenient way to receive their money and manage it.

Any efforts aimed at increasing financial inclusion must consider the financial capability of new users. Approximately, half of unbanked adults in Ethiopia state that they are unable to use an account independently. Therefore, ensuring that financially inexperienced adults can make use of such accounts for their benefit requires effective onboarding processes and product education, all in an environment that provides robust consumer protection measures.

RELATED NEWS

eTrade for Women is an initiative led by UN Trade and Development (UNCTAD), in collaboration with eTrade for all partners.

Keep in touch

Subscribe to our Newsletter

Get the eTrade for all monthly newsletter packed with our partners latest news, including on gender and the digital economy.

SUBSCRIBE