Pioneering research by The MetLife Foundation, Cenfri, UNCDF, UNSGSA, FSDK, and FSDZ (among others) on financial health has significantly increased doubt that bank and mobile money accounts alone are particularly meaningful for most people in the developing world. Access to formal financial services is generally considered an intermediate step towards meaningful outcomes like an improved ability to cover daily expenses, deal with unforeseen shocks, and effectively manage debt.

However, the body of evidence on this is quite mixed from randomized controlled trials (RCT)s that show increased consumption and consumption smoothing as a direct result of using mobile money, to RCTs that show no increase in savings or reduction in poverty and surveys that show negative correlations between increased formal account usage and financial health.

The term financial inclusion has become so confused in the literature, that many have abandoned it and are redefining impact through terms like financial health and financial wellbeing that have arrays of indicators. While these indicators make sense from a developmental impact perspective, they are difficult to measure and cannot be assessed from the GSMA dataset. However, this supply-side data does offer a useful perspective on what people use mobile money for and how useful they find it. Deeper analysis requires demand-side data, which will be available in the forthcoming Global Findex and UNCDF hopes to revisit this topic then.

Three Out of Four with Access Do Not Use Mobile Money

The last global demand side study for financial services (Global Findex) was done in 2017 by the World Bank and showed that only 4% of adults globally had mobile money accounts after about a decade of sector expansion. Whether this statistic is high/low or meaningful, depends on the analysis one is conducting. It is not very meaningful for this discussion as adults in many countries do not need mobile money services as they have superior options, and half the countries in the world do not even have a provider that offers the service.

It is more useful to examine places where mobile money is used, and its highest use is in low-income countries, where 18% of adults had a mobile money account in 2017. The model for mobile money was forged in Kenya, and the service is really designed to integrate seamlessly into informal cash-based economies. Those are the places where customers have found it valuable. The GSMA data helps understand the degree to which mobile money is useful in the places where it is used.

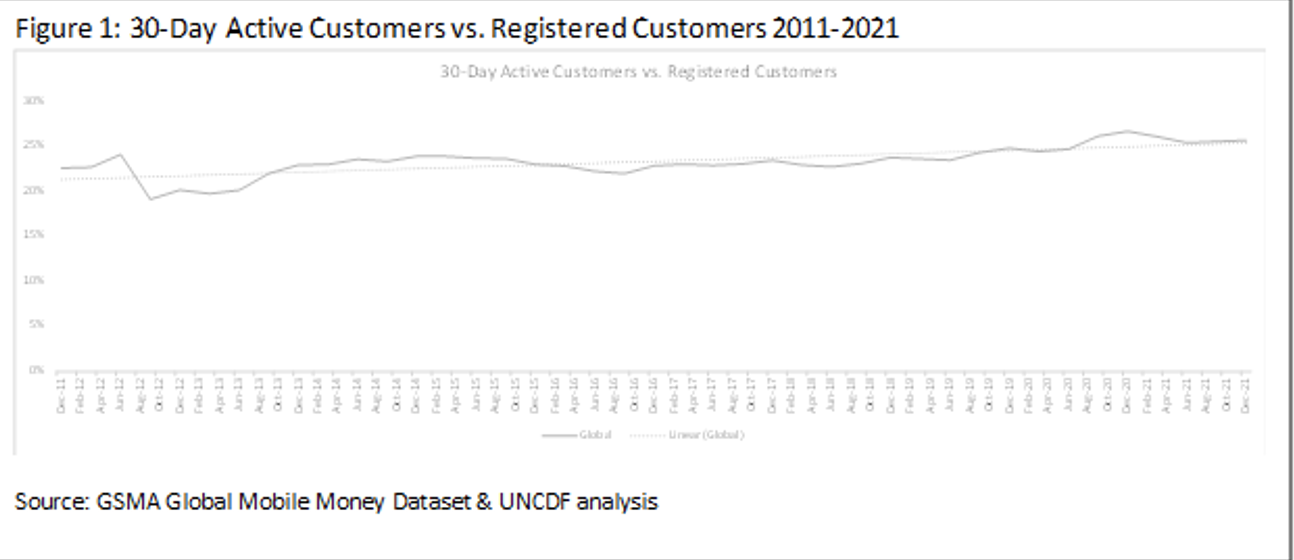

Assuming registered customers have access to mobile money is reasonable. The GSMA data shows that consistently over the last ten years, on average, 73%-81% of customers that were registered for mobile money did not make a single monthly transaction. This insight needs to be interpreted in juxtaposition to the goal to extend access to finance for all. Often, access to finance alone is not enough to inspire usage.

And while it is true that many still do not have access to mobile money accounts, this shows that for approximately three out of four people who likely do have access, they either hardly ever or possibly never use it. This seems to counterpoint assumptions that mobile money, on its own, alleviates poverty, transforms lives or is a solution to a commonly held problem for most people. It is likely only a component of solutions that strive to improve market efficiency and resilience in informal cash-based economies.

Mobile Money Usage is Limited to Six Products

Despite services like mobile money not being for everybody, there were still almost 350 million customers active on a 30-day basis at the end of 2021. While we showed in the last article that this growth rate has slowed significantly over the past years, it is still quite positive and robust, and all these statistics should be lauded by the mobile money and financial inclusion communities that have worked so hard to achieve them. It is also important to evaluate what these 350 million people are using the service for, as it has implications from a revenue standpoint, a systems evolution angle, and an impact perspective.

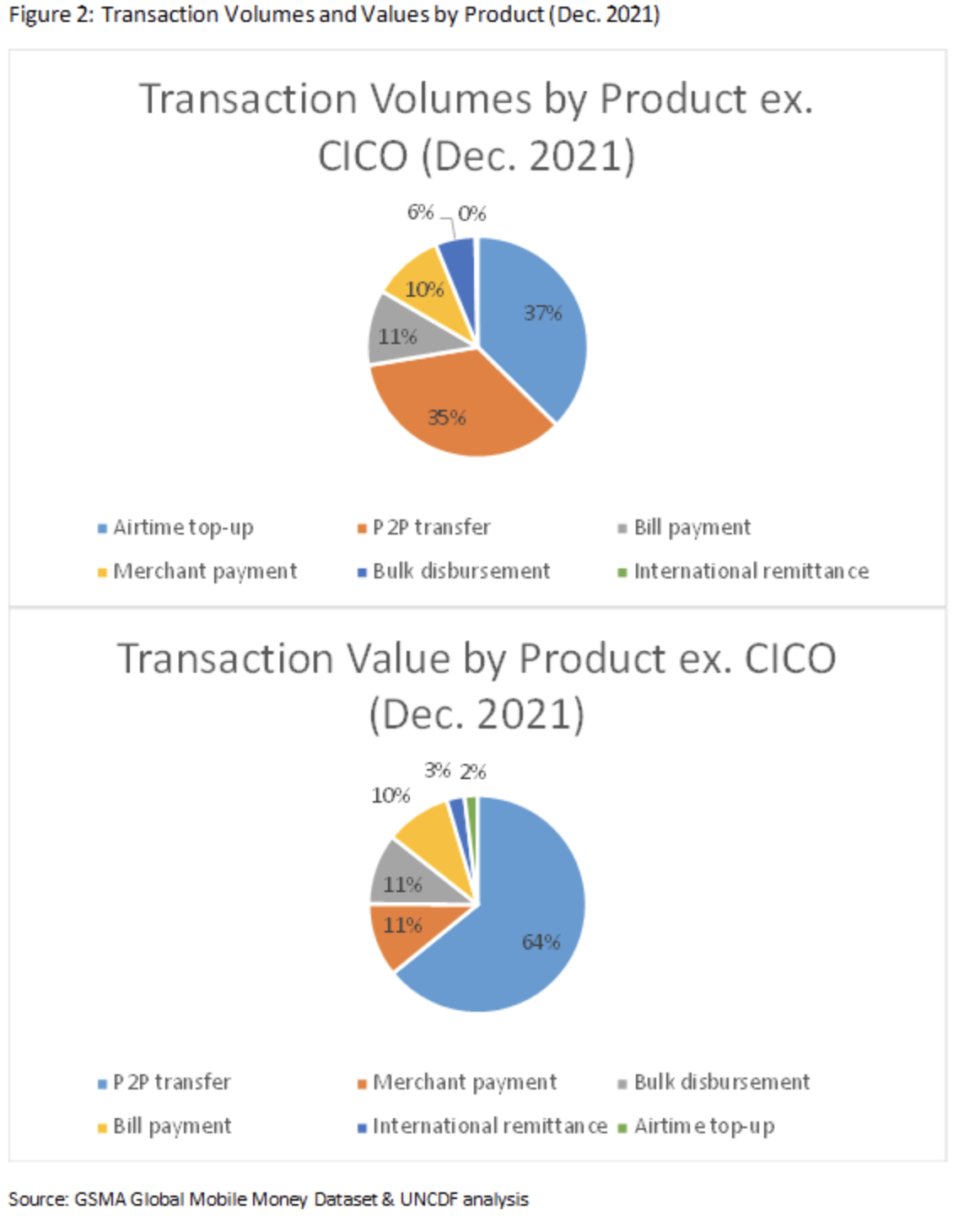

This analysis uses both the number of transactions made (volumes) and the amount of money transacted (values) for each mobile money product to measure their relative importance to the system. Cash-in and cash-out (CICO) transactions, which are 28% of volumes and 42% of values are excluded as they are not product-level transactions. t is worth noting that after 15 years of product development there are still only six product lines, showing limited innovation in the ecosystem.

Further, the pie charts in Figure 2 show that from a volumes perspective there are only four products of note, and the top two, airtime and P2P together account for 72% of volumes. The story is similar from a values perspective since there are again only four significant products and P2P itself accounts for almost two-thirds of transaction value. However, from a values perspective, merchant payments and bulk payments have surpassed bill pay as a use case, which is notable.

Mobile Money Product Suite is Evolving, But Slowly

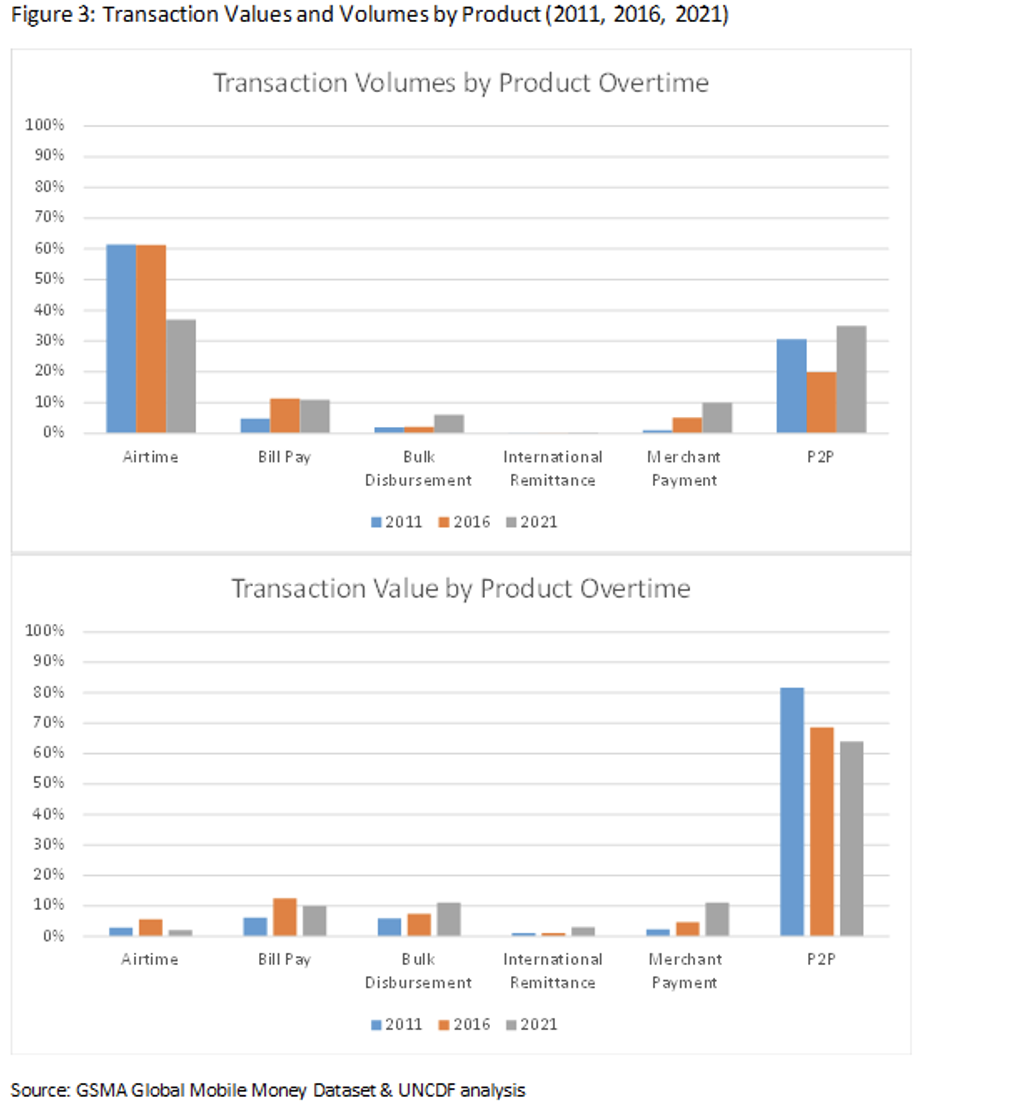

The importance of a product depends on why it is being analyzed. Some may be important from a profit perspective, but not provide much impact for customers or only for customers wealthy enough to benefit from it, limiting its impact from a financial inclusion perspective. Some products, like P2P, we expect to decline as the mobile money system evolves, while others like merchant payments will determine whether mobile money can remain relevant in the digital era. To visualize product suite evolution, the next charts present five-year snapshots over the last 10 years (2011, 2016, 2021). Figures shown are percentages of the product suite from the corresponding year.

From an evolution perspective, airtime volumes have declined significantly, as have P2P transaction values. These trends are likely to continue as 3rd party providers increasingly sell airtime, and other emerging product categories erode the relevance of the P2P as a ‘catch-all’ function. The small yet steady growth of bulk payments and merchant payments are encouraging. However, bulk payments must solve its unidirectional flow issue to scale. Mobile money is designed for balanced flows into and out of the system, and bulk payments are unidirectional flows, which break the liquidity balancing mechanisms. This system will likely need to be redesigned for significant growth.

Merchant payments are very important from a systems evolution perspective as they are the most common customer transaction type, but they still account for a very small proportion of mobile money transactions. Growth has begun as the value proposition for the merchant has been cracked in some cases. However, it is unclear how deeply into the MSME category merchant payments will penetrate beyond some select verticals like petrol stations and restaurants. Bill payments started with strong growth a while back but may have leveled off, and international remittances remain a frustratingly difficult product to scale.

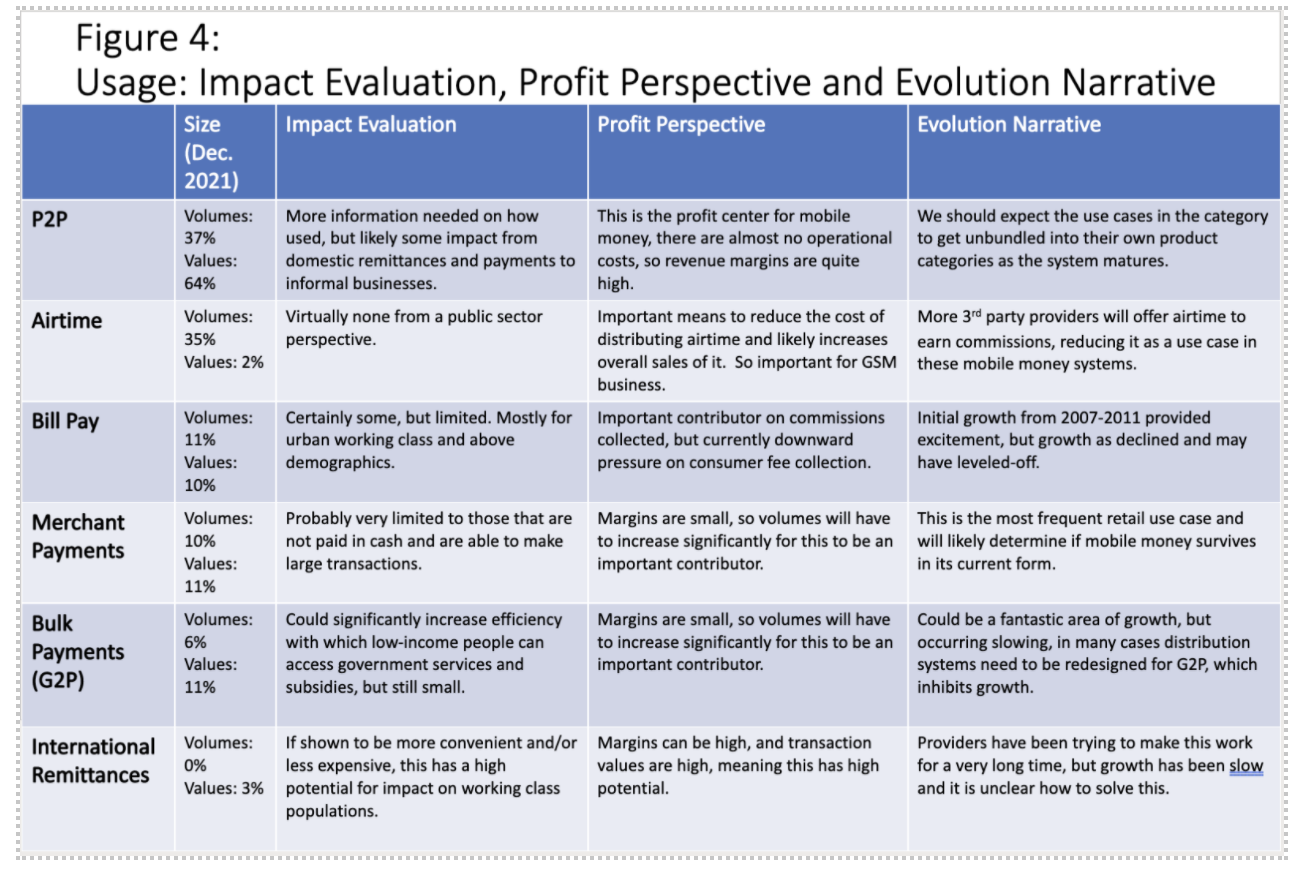

From an impact perspective, much has been written about the ability of domestic remittances to increase financial resilience, for which there is supportive evidence. However, P2P is a generic tool that customers use to solve many different issues, and it has never been well teased apart. Many describe it as a mechanism for domestic remittances from cities to rural areas.

However, data from the Helix Institute showed that the float and cash needs of agents did not match that narrative, and astute observers and long-time users understand much of this category is payments for services in the informal economy, and settling accounts within families and friends. To really understand the impact of P2P, we must first better understand how people use it.

The same is true for bill pay and bulk payments (G2P), especially since we know a portion of these categories is gambling, but we do not understand how much. In theory, G2P payments certainly have a high potential for impact, as they could make the delivery of government services and subsidies to low-income populations much more convenient and cost-effective, but they have struggled to scale.

For bill pay, it is unclear why growth has decelerated over the last five years, but it could be because this product is mostly for urban working class and wealthier families that can afford to have utilities, and those populations are relatively small and now served. While bill pay may generally not be designed for low-income populations, it has supported the evolution of selected businesses models like Pay-as-you-Go (PAYG) solar and smart device financing as well as school fee payments, which do have real impact.

Similarly, merchant payments are currently not for most people. For most adults in the developing world that earn cash and spend cash in small amounts close to their residence, the value proposition of merchant payments has yet to be articulated. Lastly, international remittances have the potential to be impactful for the portions of adults in the developing world that use them, if mobile money systems can make them less expensive and more convenient. However, the above figures show that this is still being solved as the service is seldomly used.

In conclusion, most impact narratives for mobile money discuss P2P payments as an anchor product that allow providers to earn revenue, garner a significant customer base, and then evolve a more sophisticated suite of products. Over the last 15 years, that has happened to some degree, but innovation has been quite limited and growth in other product categories has been slow. This weakens the narrative that mobile money is a gateway to product offerings in other categories that could offer more impact to customers.

The landscape changes when we include products developed by technology companies that could be delivered through mobile money systems. However, innovation from these stakeholders has been limited by the difficultly of partnering with the very mobile money systems that stand to benefit from them and are needed to enable their scale.

Even Active Mobile Money Users are Not Very Active

The next level of analysis focuses active users. We previously discussed how mobile money is used, but it is also important to understand how frequently. Given most people make several transactions a day in their daily lives, how many are made on a mobile money platform? Just focusing on the product level transactions (i.e. excluding CICO transactions), a 30-day active customer makes just over ten mobile money transactions a month, which is about one transaction every three days.

Examining the data by product category, that amounts to an airtime top-up and a P2P transfer about once a week, a bill payment and a merchant transaction about once a month, a bulk disbursement about once every two months, and an international remittance about once every three years. Therefore, on average, even active users do not use the service very actively.

Thus, arguments that mobile money itself is alleviating poverty or transforming lives and deserves significant public sector investment may be overextended. It is still a helpful service for many, and UNCDF supports the continued development of these systems as they can be essential to enabling people to interact with the digital economy. However, we should be circumspect about its ability to have an impact in otherwise analog environments.

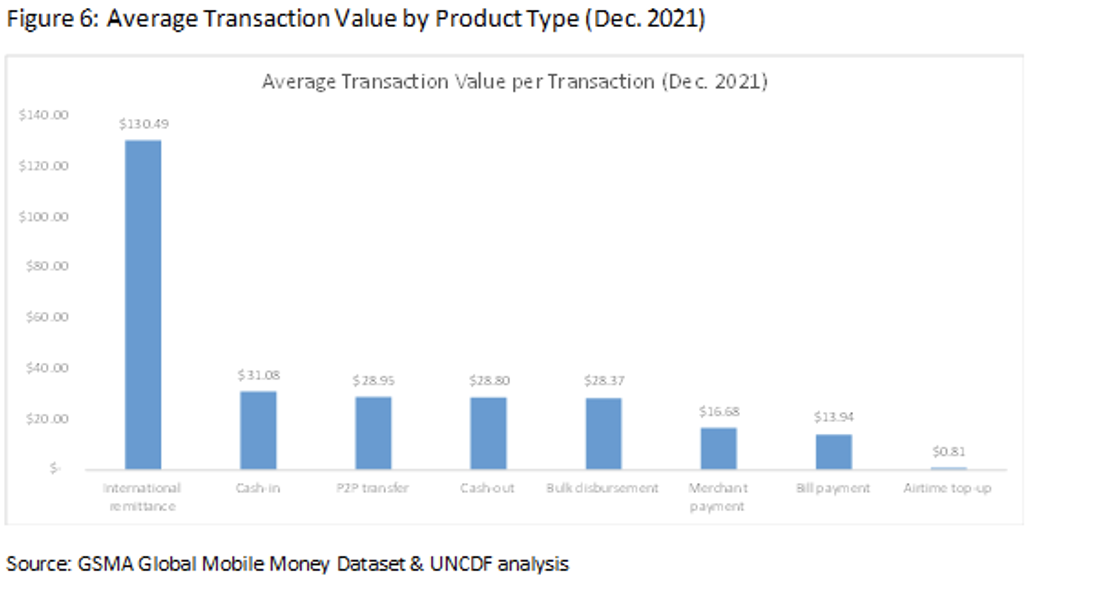

Large Average Transaction Sizes do not Indicate Impoverished Users

While the previous analysis focused on how services are used and to what degree, this final analysis examines what can be gathered about the demographics of the users from this supply side data. To do this, we analyze the value of the average transaction by product category. Again, we would have preferred to use median values to account for skewed distributions, but they are not available.

This analysis is important because the average size of the transaction may be a proxy for the income-level of the user. For small transaction values this is less likely to be true as even high-income people may make small purchases of items like airtime. However, for high value transactions it is unlikely that low-income people are conducting them, and the data reveals transaction values are surprisingly high. International remittances stand-out having an average transaction value of over US$130, indicating that on average the users are not at the bottom of the income pyramid.

Further, the average transaction values around US$30 for cash-in, cash-out, P2P, and bulk disbursements are also remarkably high. For example, in leading East African mobile money markets, this would be 45% of monthly GNI per capita in Uganda, 33% in Tanzania, and 20% in Kenya. In essence, the average adult could only afford to conduct two transactions a month of this size in Uganda, or five in Kenya. This leads to the assumption that the average mobile money user has a higher income than the average adult. This would be a different understanding than what is popularly believed in the financial inclusion community and deserves more research.

Mobile Money Improves Lives, Just Not as Much as Advertised

This analysis points out some major discrepancies in the mobile money impact narrative. Namely, it is used less, for fewer reasons, and likely by wealthier people than commonly assumed. It has also been slow to evolve. However, these are not indictments of the system. They are just reason to recalibrate our expectations of it. Mobile money has reached hundreds of millions of people who use it to make their lives easier in very tangible ways, and it is probably particularly helpful to increase resilience during disasters as money can reach the affected more easily.

The financial inclusion community should applaud these gains, and also not be satisfied by them as much work is left to do. It will involve a new cadre of builders that use technology to better customize products and integrate them into the digital economy, and it will require the financial inclusion community to embrace an improved set of metrics to measure their impact. Future solutions may ride on these mobile money payments channels or just be inspired by lessons learned from building them. Either way, mobile money has pioneered mass-market finance in many developing countries. Its legacy should be celebrated, and its impacts accurately understood to drive further innovation.

Note to Reader: This article is part of a #MobileMoney Mysteries series that uses the last 15 years of mobile money data provided by GSMA to reflect on progress in the sector and gauge where we are in answering some of the big questions still being debated.